A Thirty-Yr Journey: Charting The Historic Fluctuations Of 30-Yr Mounted Mortgage Charges

A Thirty-Yr Journey: Charting the Historic Fluctuations of 30-Yr Mounted Mortgage Charges

Associated Articles: A Thirty-Yr Journey: Charting the Historic Fluctuations of 30-Yr Mounted Mortgage Charges

Introduction

With enthusiasm, let’s navigate via the intriguing subject associated to A Thirty-Yr Journey: Charting the Historic Fluctuations of 30-Yr Mounted Mortgage Charges. Let’s weave fascinating info and provide recent views to the readers.

Desk of Content material

A Thirty-Yr Journey: Charting the Historic Fluctuations of 30-Yr Mounted Mortgage Charges

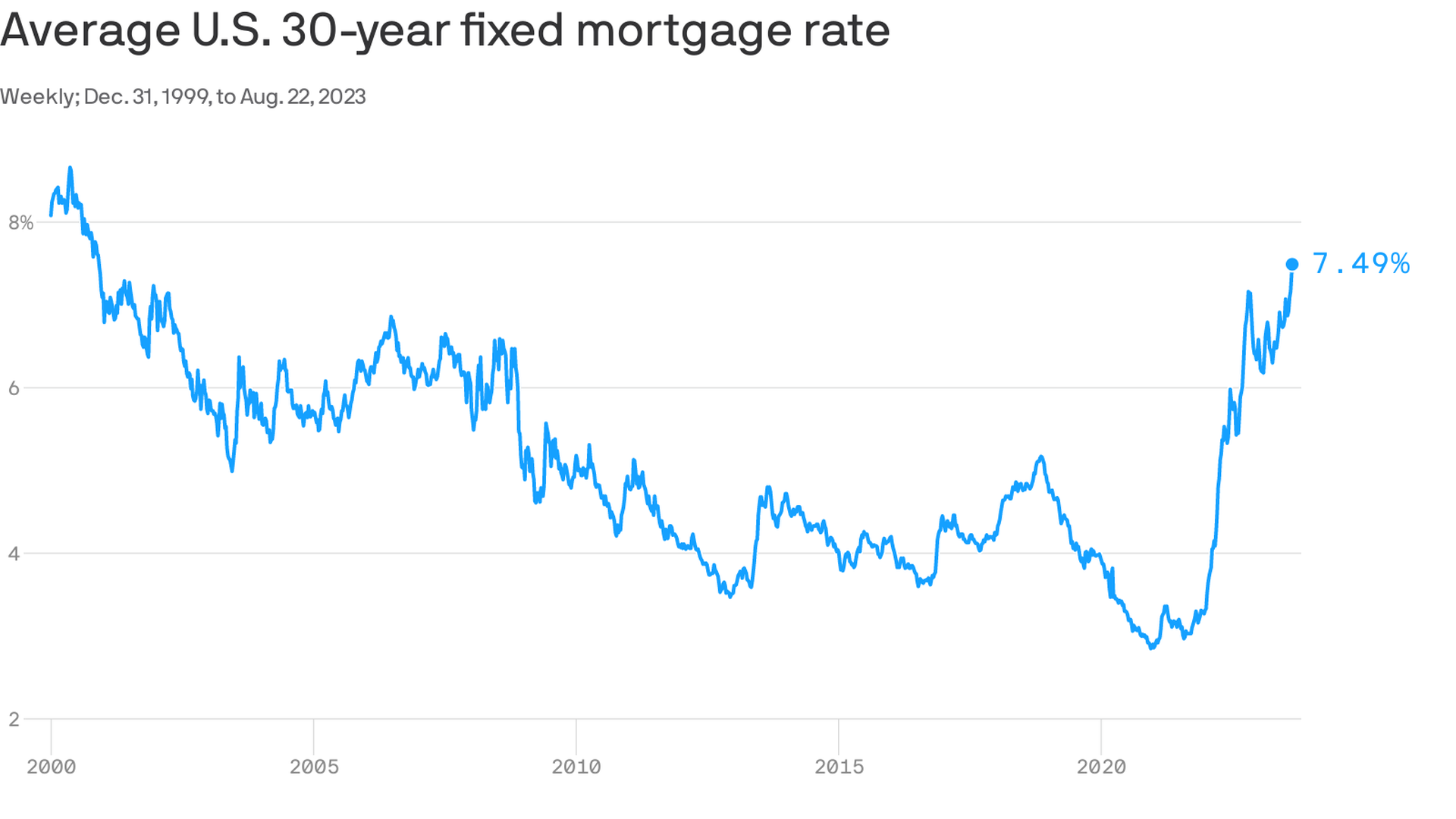

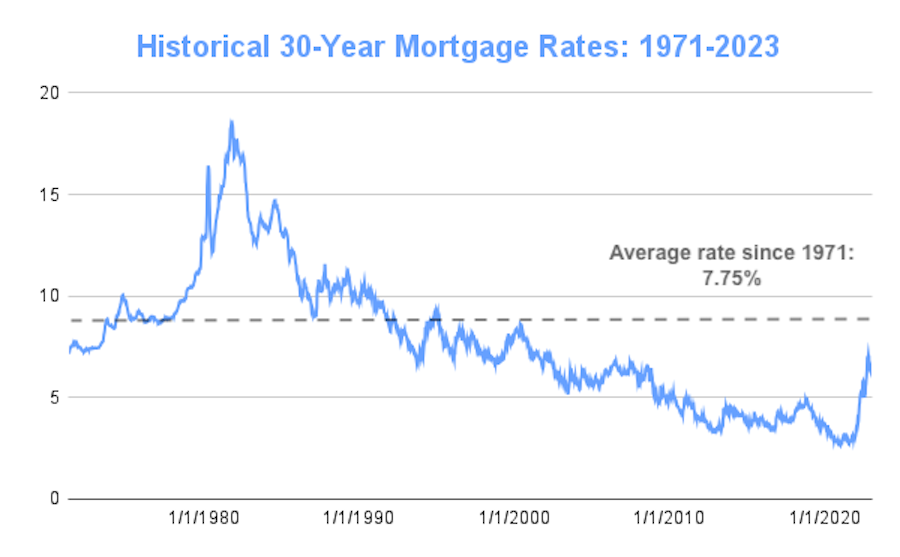

The 30-year fixed-rate mortgage (FRM) is the cornerstone of the American dream of homeownership. For many years, it has supplied debtors the steadiness of a predictable, long-term cost, shielding them from fluctuating rates of interest. Nevertheless, the rate of interest itself is much from static, present process dramatic shifts all through historical past. Understanding these historic fluctuations, as depicted in a 30-year fastened mortgage charges historic chart, is essential for potential homebuyers, actual property traders, and anybody within the broader financial panorama.

This text delves into the historic developments of 30-year FRM charges, analyzing key durations of great change and exploring the underlying financial forces which have formed them. We’ll look at the info introduced in a hypothetical historic chart (as real-time knowledge fluctuates always), highlighting pivotal moments and providing context for future predictions. Whereas exact numbers will range relying on the supply and methodology used, the general developments stay constant and informative.

A Hypothetical Historic Chart: Understanding the Visible Narrative

Think about a line graph, our hypothetical historic chart, spanning a number of a long time, maybe from 1970 to the current. The horizontal axis represents time (years), whereas the vertical axis denotes the common annual 30-year FRM rate of interest (expressed as a proportion). This chart would instantly reveal a captivating story of booms, busts, and long-term developments.

Key Intervals of Curiosity:

-

The Seventies and Early Nineteen Eighties: The Period of Excessive Inflation and Excessive Charges: This era is characterised by a dramatic upward surge in mortgage charges. Double-digit inflation, fueled by elements just like the oil disaster, pressured the Federal Reserve to implement tight financial insurance policies, considerably growing rates of interest throughout the board. The chart would present charges peaking within the mid-teens, making homeownership a big monetary burden for a lot of. This period highlights the crucial relationship between inflation and mortgage charges – excessive inflation invariably results in larger borrowing prices.

-

The Mid-Nineteen Eighties to the Early 2000s: A Gradual Decline and Relative Stability: Following the aggressive rate of interest hikes of the earlier decade, the chart would illustrate a gradual, albeit uneven, decline in mortgage charges. This era witnessed financial growth, technological developments, and elevated monetary deregulation, all contributing to decrease charges. Whereas there have been fluctuations, the general development was downward, making homeownership extra accessible to a wider section of the inhabitants. This period additionally noticed the rise of mortgage-backed securities and the growing complexity of the mortgage market.

-

The Mid-2000s Housing Growth and Bust: The chart would dramatically illustrate the fast decline in charges main as much as the housing increase of the mid-2000s. Extraordinarily low rates of interest, coupled with lax lending requirements (subprime mortgages), fueled a speculative frenzy within the housing market. This era noticed charges dip to traditionally low ranges, resulting in an unprecedented surge in residence costs and mortgage lending. The next collapse of the housing market, triggered by the bursting of the housing bubble, is vividly depicted by a pointy upward swing in charges as lenders tightened credit score and the financial system spiraled into recession. This era serves as a cautionary story of the hazards of unchecked progress and unsustainable lending practices.

-

The Publish-2008 Period: Close to-Zero Charges and Gradual Restoration: Within the wake of the 2008 monetary disaster, the Federal Reserve applied a coverage of near-zero rates of interest to stimulate financial progress. The chart would present a dramatic plunge in mortgage charges to traditionally low ranges, even dipping beneath 4% in some durations. This coverage, whereas efficient in stopping a deeper financial collapse, additionally contributed to a interval of sluggish financial restoration and considerations about asset bubbles in different sectors. The next gradual enhance in charges displays the Fed’s makes an attempt to normalize financial coverage.

-

Current Developments and Future Predictions: The newest part of the chart would illustrate the continued fluctuations in mortgage charges, influenced by elements like inflation, financial progress, geopolitical occasions, and Federal Reserve coverage. Predicting future developments is inherently difficult, however analyzing previous patterns and present financial indicators can present some perception. Components comparable to inflation, the Federal Reserve’s financial coverage selections, and international financial situations will proceed to play a big function in shaping future mortgage charges.

Components Influencing 30-Yr Mounted Mortgage Charges:

A number of key elements work together to find out the prevailing 30-year FRM price:

-

Federal Reserve Coverage: The Federal Reserve’s financial coverage, notably its goal federal funds price, considerably influences mortgage charges. When the Fed raises rates of interest to fight inflation, mortgage charges usually comply with swimsuit. Conversely, price cuts aimed toward stimulating financial progress often result in decrease mortgage charges.

-

Inflation: Excessive inflation erodes the buying energy of cash, main central banks to lift rates of interest to manage worth will increase. This, in flip, impacts mortgage charges.

-

Financial Progress: Sturdy financial progress typically results in larger rates of interest as demand for credit score will increase. Conversely, weak financial progress typically ends in decrease charges.

-

Provide and Demand for Mortgages: The general provide and demand dynamics within the mortgage market additionally have an effect on charges. Elevated demand for mortgages can push charges larger, whereas decreased demand can result in decrease charges.

-

World Financial Circumstances: World financial occasions, comparable to worldwide crises or shifts in international capital flows, also can affect mortgage charges.

-

Authorities Rules: Authorities rules impacting the mortgage market, comparable to modifications in lending requirements or necessities for mortgage-backed securities, can affect charges.

The Significance of Understanding Historic Developments:

Understanding the historic fluctuations depicted in a 30-year fastened mortgage charges historic chart is essential for a number of causes:

-

Knowledgeable Choice-Making: Potential homebuyers can use historic knowledge to achieve a greater understanding of the potential vary of mortgage charges and make extra knowledgeable selections about when to buy a house.

-

Threat Evaluation: Buyers in actual property can use historic knowledge to evaluate the dangers related to mortgage-backed securities and different mortgage-related investments.

-

Financial Forecasting: Economists and monetary analysts can use historic knowledge to develop fashions for forecasting future mortgage charges and their affect on the broader financial system.

-

Coverage Formulation: Policymakers can use historic knowledge to tell selections about financial coverage and rules impacting the mortgage market.

Conclusion:

The 30-year fastened mortgage price has a wealthy historical past, reflecting the ebb and circulation of the broader financial system. Analyzing a historic chart of those charges reveals a compelling narrative of booms, busts, and the advanced interaction of financial forces. By understanding these previous developments and the elements that affect them, people, traders, and policymakers could make extra knowledgeable selections about homeownership, funding methods, and financial coverage. Whereas predicting the longer term is not possible, finding out the previous gives invaluable context for navigating the ever-changing panorama of the mortgage market. The journey of the 30-year FRM price is a testomony to the dynamic nature of the financial system and the enduring significance of understanding its historic trajectory.

Closure

Thus, we hope this text has offered helpful insights into A Thirty-Yr Journey: Charting the Historic Fluctuations of 30-Yr Mounted Mortgage Charges. We hope you discover this text informative and useful. See you in our subsequent article!