Decoding The three-Month Euribor: A Deep Dive Into The Eurozone’s Key Curiosity Price

Decoding the 3-Month Euribor: A Deep Dive into the Eurozone’s Key Curiosity Price

Associated Articles: Decoding the 3-Month Euribor: A Deep Dive into the Eurozone’s Key Curiosity Price

Introduction

With nice pleasure, we are going to discover the intriguing matter associated to Decoding the 3-Month Euribor: A Deep Dive into the Eurozone’s Key Curiosity Price. Let’s weave attention-grabbing info and supply recent views to the readers.

Desk of Content material

Decoding the 3-Month Euribor: A Deep Dive into the Eurozone’s Key Curiosity Price

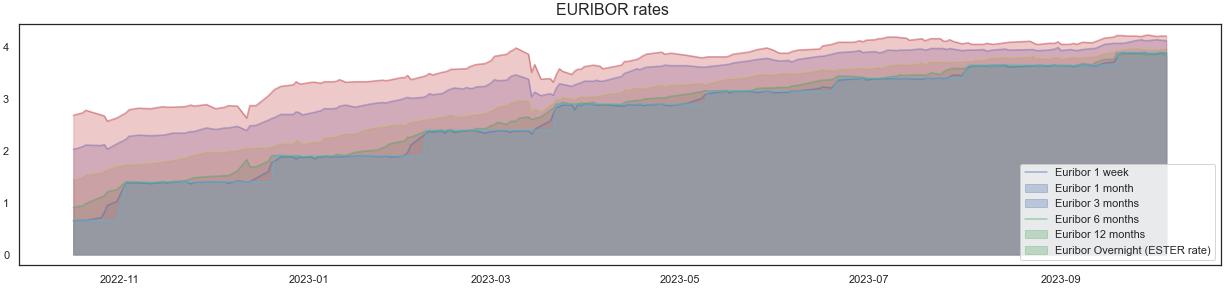

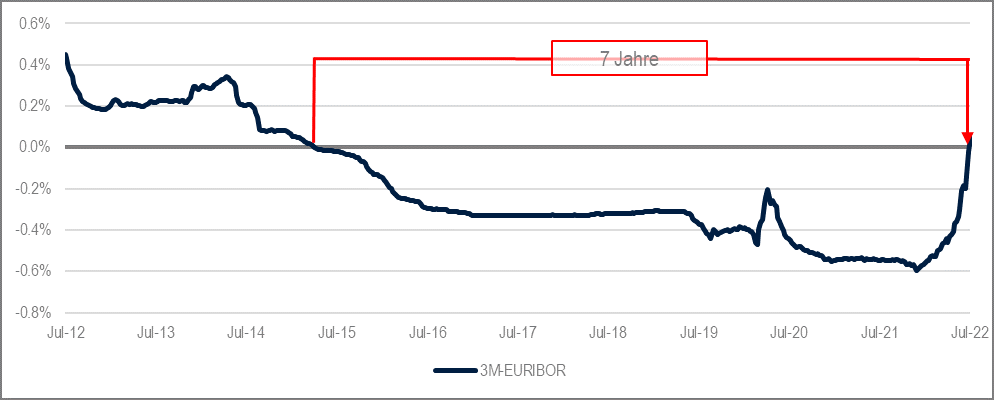

The three-month Euribor (Euro Interbank Supplied Price) is an important benchmark rate of interest within the Eurozone, reflecting the typical rate of interest at which banks lend unsecured funds to one another for a three-month interval. Understanding its fluctuations is significant for anybody concerned within the Eurozone’s monetary markets, from companies managing their borrowing prices to traders assessing danger and return. This text will delve into the intricacies of the 3-month Euribor, exploring its historic context, calculation methodology, influencing elements, and its significance for varied market members.

Historic Context and the Shift to ESTR:

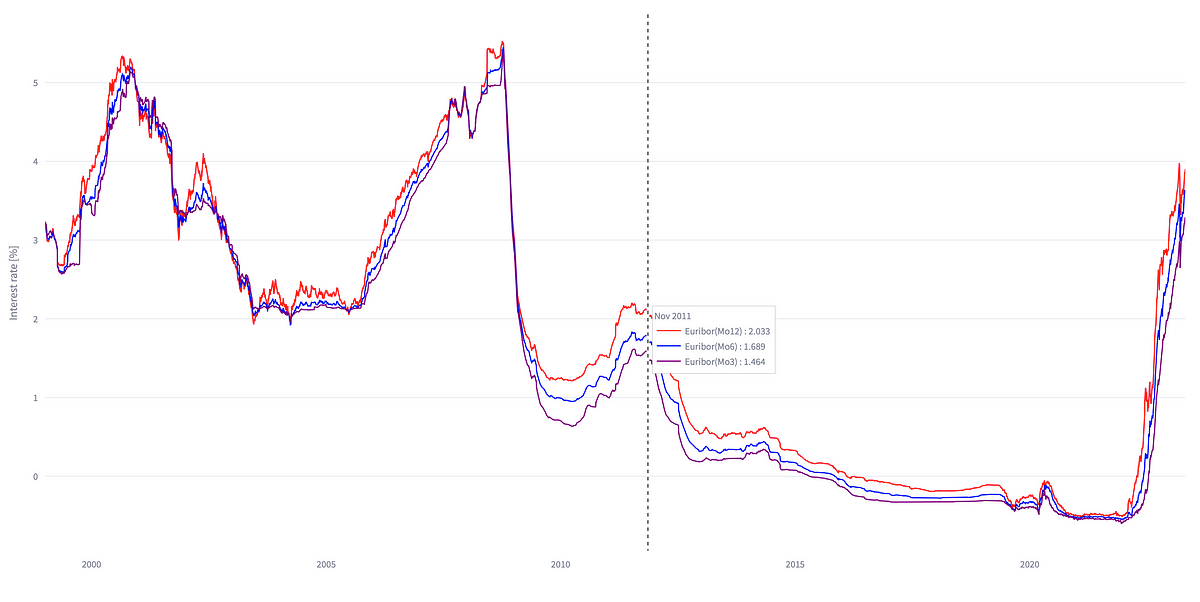

The Euribor, in its varied tenors (starting from in a single day to 12 months), has been a cornerstone of the Eurozone’s monetary system since its inception in 1999. It serves as a reference price for an enormous array of monetary merchandise, together with:

- Loans: Mortgages, company loans, and client loans often use Euribor as a benchmark for variable rates of interest.

- Derivatives: A variety of rate of interest swaps, futures, and choices are priced relative to Euribor.

- Bonds: Some bonds use Euribor as a reference price for coupon funds or principal repayments.

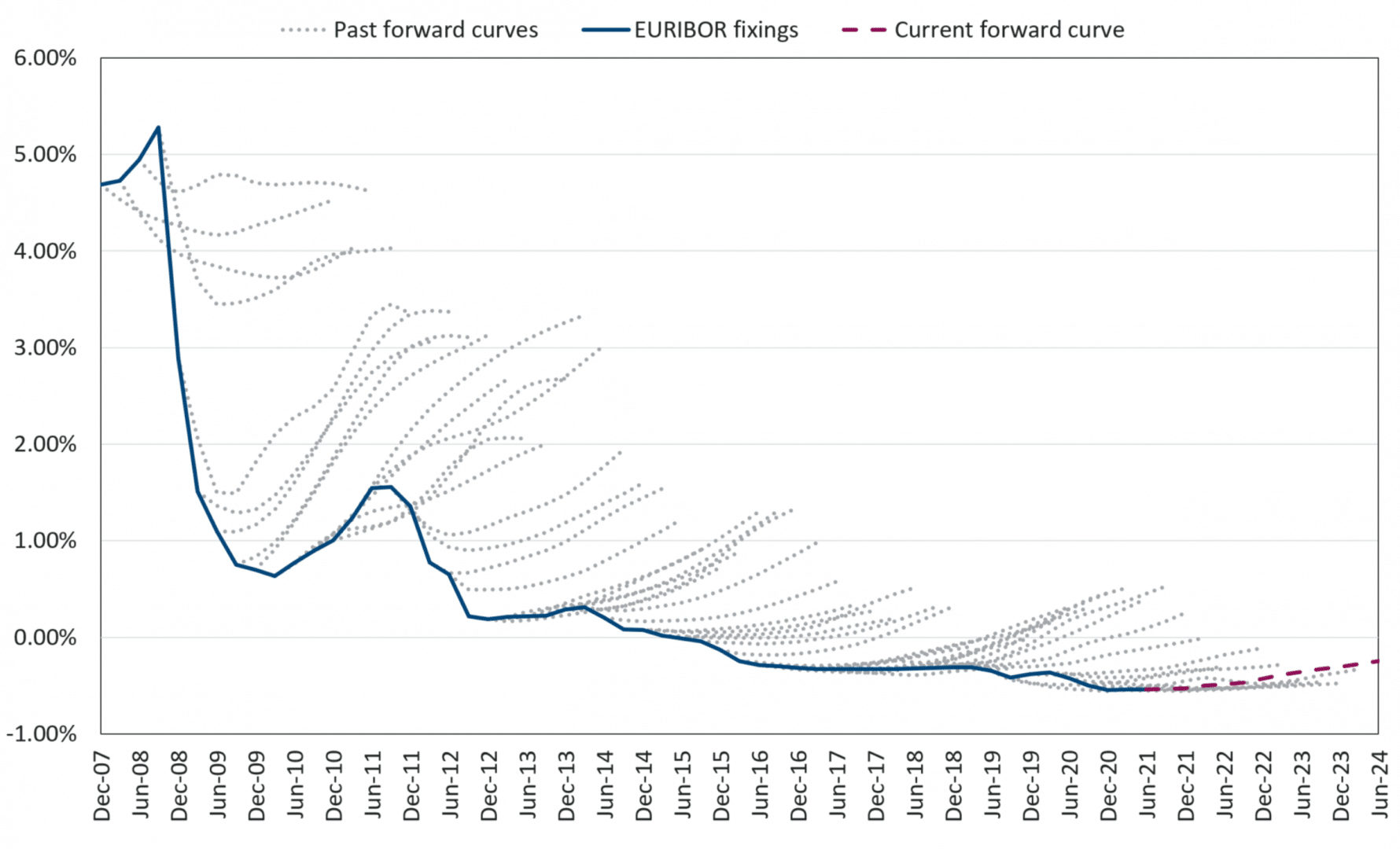

Nonetheless, the Euribor’s methodology confronted criticism regarding its susceptibility to manipulation and its lack of robustness during times of market stress. This led to the event of the Euro Quick-Time period Price (€STR), a reformulated benchmark price designed to handle these shortcomings. The €STR is predicated on precise transactions within the in a single day unsecured market, providing a extra dependable and clear illustration of interbank borrowing prices. Whereas the €STR is step by step changing Euribor as the first benchmark, understanding Euribor’s historic habits stays essential, notably for legacy contracts nonetheless referencing it. The transition from Euribor to €STR is a posh course of, with many contracts nonetheless referencing Euribor for a number of years to return.

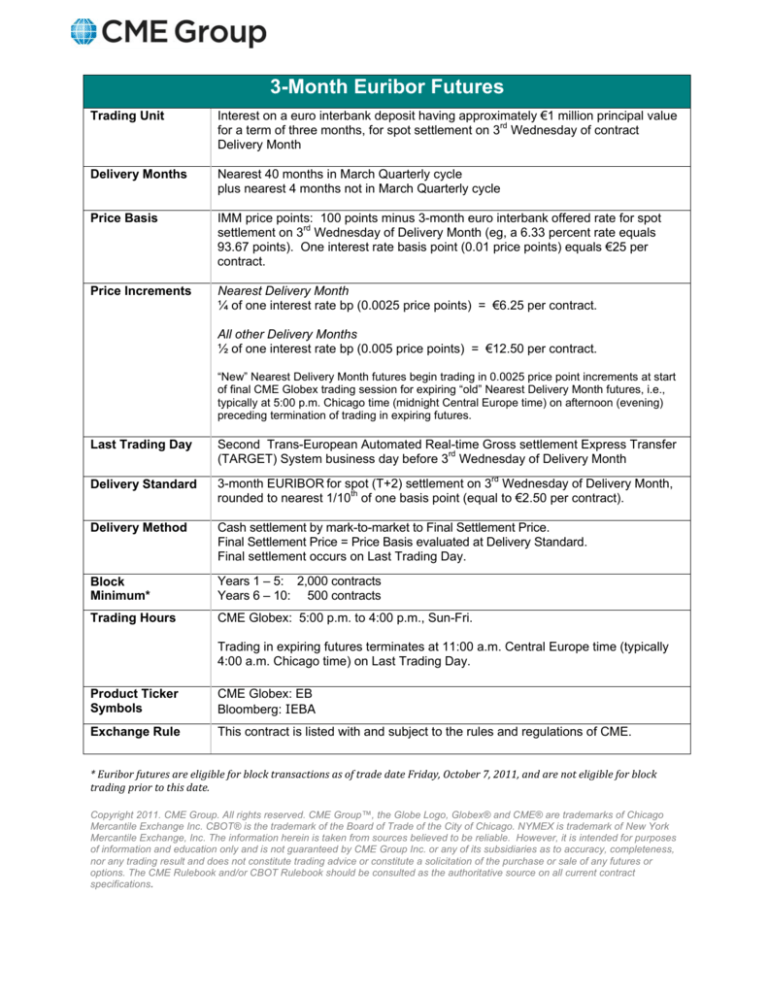

Calculation Methodology (Pre-€STR Period):

Earlier than the €STR’s introduction, the 3-month Euribor was calculated day by day by the European Cash Markets Institute (EMI), based mostly on the submitted rate of interest contributions from a panel of contributing banks. The calculation concerned:

- Panel Choice: A panel of main banks within the Eurozone submitted their estimated borrowing prices for 3-month unsecured loans.

- Information Assortment: Every financial institution submitted its price, representing the rate of interest at which it may borrow funds from different banks.

- Outlier Elimination: The EMI would determine and take away outlier charges, thought-about to be unusually excessive or low in comparison with the general distribution. The factors for outlier removing had been based mostly on statistical strategies designed to eradicate information factors which may distort the typical.

- Weighted Common Calculation: The remaining charges had been then averaged, typically utilizing a weighted common to replicate the relative significance of every contributing financial institution out there. The weighted common represented the ultimate 3-month Euribor price.

This technique, whereas seemingly simple, was prone to manipulation, as banks had an incentive to submit charges that favored their very own pursuits. This vulnerability contributed to the push for a extra strong and clear benchmark price just like the €STR.

Components Influencing the 3-Month Euribor:

Quite a few elements affect the 3-month Euribor, reflecting the complicated interaction of financial and financial forces inside the Eurozone:

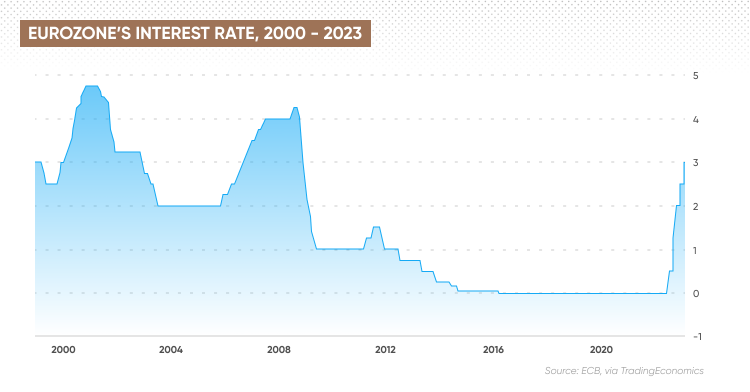

- European Central Financial institution (ECB) Financial Coverage: The ECB’s key rates of interest, notably the primary refinancing operations (MRO) price, are probably the most vital driver of Euribor. When the ECB raises rates of interest, it turns into dearer for banks to borrow funds, resulting in a rise in Euribor. Conversely, rate of interest cuts by the ECB sometimes translate into decrease Euribor charges.

- Inflation: Excessive inflation pressures typically immediate the ECB to tighten financial coverage, resulting in larger Euribor charges. Conversely, low inflation might enable the ECB to keep up and even decrease rates of interest, leading to decrease Euribor.

- Financial Development: Sturdy financial progress can result in elevated demand for credit score, doubtlessly pushing Euribor upwards. Conversely, weak financial progress may scale back credit score demand and exert downward stress on Euribor.

- Authorities Debt Ranges: Excessive ranges of presidency debt in Eurozone international locations can enhance uncertainty and danger aversion amongst banks, doubtlessly resulting in larger borrowing prices and a better Euribor.

- World Financial Situations: World financial shocks, reminiscent of monetary crises or geopolitical occasions, can have an effect on investor sentiment and danger urge for food, influencing the interbank lending market and impacting Euribor.

- Liquidity within the Interbank Market: The supply of liquidity within the interbank market performs a vital position. Durations of tight liquidity can result in larger borrowing prices and a better Euribor.

- Regulatory Modifications: Modifications in banking laws can influence the associated fee and availability of funds for banks, influencing Euribor.

Significance for Market Individuals:

The three-month Euribor (and its successor, €STR) has far-reaching penalties for a variety of market members:

- Debtors: Companies and people with variable-rate loans see their borrowing prices instantly influenced by Euribor actions. A rising Euribor will increase their month-to-month funds, whereas a falling Euribor reduces them.

- Lenders: Banks and different monetary establishments providing variable-rate loans see their profitability affected by Euribor modifications. A rising Euribor will increase their revenue margins, whereas a falling Euribor reduces them.

- Traders: Traders in rate of interest derivatives and bonds priced relative to Euribor face features or losses relying on the course of Euribor actions.

- Hedgers: Companies and monetary establishments use Euribor-linked derivatives to hedge in opposition to rate of interest danger, defending themselves from hostile actions in Euribor.

- Central Banks: The ECB displays Euribor intently as an indicator of financial coverage effectiveness and the general well being of the Eurozone banking system.

The Transition to €STR and its Implications:

The transition from Euribor to €STR marks a big shift in the direction of a extra strong and dependable benchmark price. The €STR, based mostly on precise in a single day transactions, is much less prone to manipulation and gives a extra correct reflection of interbank borrowing prices. Nonetheless, the transition is a gradual course of, and lots of contracts proceed to reference Euribor for a number of years. This necessitates cautious monitoring of each charges and understanding the implications of the transition for varied monetary devices. The legacy of Euribor information, nonetheless, stays very important for historic evaluation and understanding long-term traits within the Eurozone’s interbank market.

Conclusion:

The three-month Euribor, regardless of its eventual alternative by the €STR, stays a big benchmark rate of interest with a wealthy historical past and profound implications for the Eurozone economic system. Understanding its historic habits, calculation methodology, influencing elements, and its position in varied monetary markets is essential for navigating the complexities of the Eurozone’s monetary panorama. Whereas the €STR presents a extra strong and clear different, the legacy of Euribor and the continued transition interval require cautious consideration for all market members. The way forward for rate of interest benchmarking within the Eurozone rests on the continued success and widespread adoption of the €STR, making certain a extra resilient and dependable monetary system.

![Geldanlage für 3 Jahre [Vergleich 2023] DeltaValue](https://www.deltavalue.de/wp-content/uploads/2021/08/3-monats-euribor-chart-1024x626.png)

Closure

Thus, we hope this text has offered useful insights into Decoding the 3-Month Euribor: A Deep Dive into the Eurozone’s Key Curiosity Price. We admire your consideration to our article. See you in our subsequent article!